Will insurance go up after a speeding ticket in Florida?

will insurance go up after speeding ticket? Discover how Florida violations affect your rates and how to protect your premiums.

Let's be blunt: a speeding ticket in Florida can hit you where it hurts—your wallet. And not just with the initial fine. The real pain often comes from your insurance company, which will almost certainly review your record. A single ticket can trigger a premium hike that sticks around for years, potentially costing you hundreds, if not thousands, of dollars long after you've paid the court.

The Unmistakable Impact of a Speeding Ticket on Florida Insurance

Think of a speeding ticket as more than just a roadside inconvenience. It's a financial event with a long tail. For anyone driving on busy routes like I-95 in Broward County, one heavy foot can lead directly to a sustained jump in your auto insurance bill. Before we get into the nitty-gritty, it helps to understand how the insurance industry sees things. To them, a speeding violation is a bright red flag that signals "increased risk," and they may adjust your premium to match.

This isn't just a tiny bump, either. Florida drivers can face one of the steepest average rate increases in the entire country after just one speeding ticket. Costs can leap by a staggering $617 per year. Because Florida is a no-fault insurance state, carriers are extra cautious. They may see a driver with a recent violation as someone who's more likely to get into a future accident and file a claim.

Speeding Ticket Impact on Florida Auto Insurance: A Quick Look

To really put the cost into perspective, let's break down what a typical speeding ticket can mean for your budget over time. That initial fine you pay is often the smallest part of the total expense.

Metric | Average Cost for Florida Drivers |

|---|---|

Average Annual Rate Increase | $400 - $650+ |

Duration of Rate Increase | 3 to 5 Years |

Total Long-Term Cost (3 Years) | $1,200 - $1,950+ |

As you can see, the math isn't pretty. What starts as a simple ticket can snowball into a significant financial burden that may follow you for years.

How a Ticket Affects Your Record

When you get a speeding ticket in Florida and are found guilty, points get added to your driving record. Insurance companies don't just set your rate and forget it; they regularly review these records, especially when it's time to renew your policy. They use this information to reassess how risky you are to insure.

Every point acts like a demerit, signaling to the insurer that you are statistically more likely to be involved in a crash. This is precisely why navigating Florida’s points system is so critical. The more points you rack up, the higher your perceived risk, and that translates directly into more expensive car insurance.

Why Do Insurance Rates Go Up After a Ticket Anyway?

So, why does a single speeding ticket feel like it sets off an alarm at your insurance company? It's not personal, and it's definitely not a "penalty" from them. It's a business decision rooted entirely in risk assessment.

To your insurer, your driving record is basically a financial report card. A speeding ticket can be a significant mark against you.

Insurance companies live and breathe statistics. Their whole business model is built on predicting the future—specifically, how likely you are to file a claim. A speeding ticket sends a clear signal that you may be a riskier driver. Data often shows that drivers who speed are statistically more likely to get into an accident, and accidents cost insurers money.

Your Driving Record Tells the Whole Story

When you pay that ticket or are found guilty in court, the violation gets etched onto your official driving history. Here in Florida, that information is logged into the state's Driver Vehicle Information Database (DAVID). Insurers have access to this system and make a habit of checking it, usually right around the time your policy is up for renewal.

That means the ticket you got months ago down in Miami-Dade County will eventually pop up on their radar. When an underwriter sees a new violation, they may immediately recalculate your risk profile. In their eyes, you've just become more expensive to insure.

The insurance company may see a speeder as a higher-risk individual who might cause a future accident, forcing them to pay out thousands of dollars in a claim. To offset that higher risk, they raise your premiums.

This isn't some manager making a judgment call. It's an automated process crunched by actuarial tables that connect specific violations, like speeding, to the probability of future claims.

How Points Turn Into Premium Hikes

Florida’s point system adds another layer of math to the problem. When you're convicted of speeding, points get tacked onto your license. For an insurer, these points are a simple, quantifiable way to measure just how risky you've become.

Minor Violations: Going 15 mph or less over the limit will usually add 3 points.

Major Violations: Pushing it more than 15 mph over the limit can land you 4 points.

Every point signals a higher statistical chance of an accident. The more points you rack up, the riskier you look on paper, and the higher your premiums are going to climb. This is exactly why it's so important to understand Florida's speeding ticket points and what you can do to keep them off your record.

At the end of the day, it's not the ticket itself that directly jacks up your rates. It’s what the ticket represents to your insurer: proof of risky behavior and points on your record. They're just adjusting your price to match your new, higher-risk profile.

Calculating the Cost of a Florida Speeding Ticket

So, you got a speeding ticket. After the initial frustration, the big question hits: "How much is this going to cost me?" And I'm not just talking about the fine on the ticket. The real financial pain often comes from your insurance company.

But the answer isn't a simple, flat number. Think of it more like a sliding scale. A minor ticket might just nudge your rates up, but a serious one can send them higher. Insurers look at the whole picture to figure out just how much of a risk you've become.

Severity of the Violation

The single biggest factor is how fast you were going. An officer clocking you at 10 mph over the limit is one thing; getting caught doing 30 mph over is a completely different story.

Minor Speeding (e.g., 10-15 mph over): This will likely land you a more moderate rate hike, often in the 10-20% range. It's not great, but it's on the lower end of the pain scale.

Major Speeding (e.g., 25-30+ mph over): Now you're signaling a much higher level of risk. A driver caught speeding on a busy road in Broward County could see their premium jump by 30% or more.

The logic here is straightforward: the faster you're driving, the more devastating—and expensive—a potential crash becomes. Insurance companies adjust your rates to match that heightened risk.

Your Prior Driving History

What you've done in the past matters. A lot. An insurer might be more forgiving if you have a spotless decade-long driving record. It's your first mistake, and they might see it that way.

But if you already have a couple of other violations on your record from the last three to five years, this new speeding ticket just confirms a pattern of risky behavior. It’s the difference between a one-off error and a bad habit, and your premium will reflect that. Each new ticket just digs the hole a little deeper.

Your Insurance Provider's Policies

Not all insurance companies are created equal. Each one has its own proprietary methods—their own algorithms and rules for calculating risk.

Some might offer a "first ticket forgiveness" program for long-time customers with otherwise clean records. Others are stricter and will raise your rates after any moving violation, no matter how small. This is why the exact same ticket can result in wildly different premium increases depending on who your carrier is.

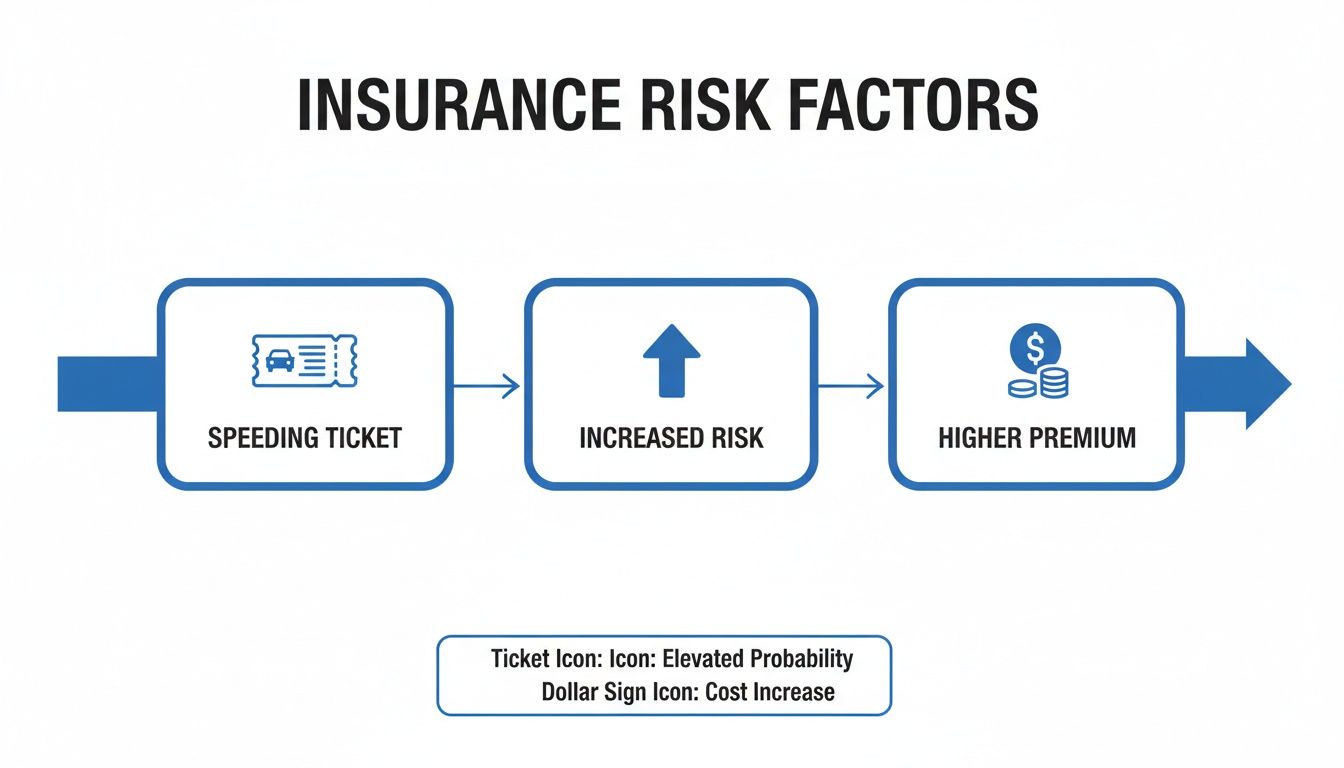

This chart breaks down the simple, but costly, chain reaction a ticket sets off.

As you can see, the ticket directly flags you as a higher risk, and higher risk can mean higher premiums.

Nationally, a single speeding ticket can increase car insurance rates by 22% to 30% on average, and Florida drivers often feel the sting. The exact amount depends heavily on your speed; getting caught going more than 15 mph over the limit can trigger rate hikes from major insurers ranging anywhere from 19% to 31%. You can get a better idea of how different speeds affect rates from top insurance providers and see just how expensive a lead foot can be.

How Long a Speeding Ticket Stays on Your Insurance Record

That rate hike from a speeding ticket isn't a life sentence for your wallet, but it definitely overstays its welcome. The key thing to understand is that insurance companies work on a "look-back" period. Think of it as the window of time they use to peek at your driving history and figure out how much of a risk you are.

For most insurers in Florida and across the U.S., this look-back period is typically three to five years. During that time, a speeding conviction is a major factor in how they calculate what you pay. Keeping your record clean inside that window is your express lane back to lower rates.

The Look-Back Period Explained

The look-back period is kind of like being on insurance probation. If you get another ticket while an old one is still visible on your record, the financial consequences can stack up fast. One ticket might just sting a little, but a second one within that three-to-five-year window can signal a pattern of risky driving. That could lead to a much steeper rate hike or even get you booted into a high-risk insurance category.

It's also crucial to know the difference between your driving record and your insurance record. Points from a ticket might fall off your Florida driver's license after a while, but the violation itself can stick around for insurers to see for much longer. You can dig into this more by exploring how long traffic tickets stay on your record in detail.

The Financial Echo of a Ticket

To an insurer, a speeding ticket suggests "high risk," triggering premium hikes that hang around for years. On average, U.S. drivers see annual increases of $480 to $648, all depending on how fast they were going. When you look past the initial fine, the insurance penalties alone can add up to more than $1,600 over that three-year look-back period.

The impact is often even bigger here in Florida, where studies point to an average yearly spike of $617. As you can see from these insights on insurance costs, that's because of factors like our state's packed roads and no-fault insurance laws.

Your insurance rate won't stay elevated forever. After the three-to-five-year look-back period passes without any new violations, you can generally expect your premiums to return to normal, reflecting your improved and safer driving history.

So You Got a Ticket. Here's How to Protect Your Insurance Premiums.

Getting a speeding ticket doesn't automatically mean your insurance rates are doomed. Far from it. By taking a few smart, proactive steps, you can seriously influence the outcome and protect your wallet. That period right after you get a citation is critical—it's when you make the decisions that can keep points off your license and your premiums right where they are.

The single most effective way to sidestep an insurance hike is to prevent the conviction from ever hitting your record. Too many Florida drivers make the mistake of just paying the fine. That's an admission of guilt, and it guarantees points and puts your insurer on alert. You have much better options.

Contest the Ticket with Legal Help

One of the most powerful strategies you can use is to contest the ticket. This doesn't mean you have to march into court and argue with a judge yourself. Retaining a traffic ticket attorney lets a professional handle the entire process for you. Our goal is always to protect your license and your record by seeking the best possible outcome.

An attorney will dig into the details of your traffic stop, looking for procedural errors or weaknesses in the officer's report. From there, they can negotiate with the prosecutor. The objective is often to get the ticket dismissed entirely or knocked down to a non-moving violation, which typically carries no points and stays off your insurance company's radar. Understanding the chances of getting a speeding ticket dismissed can give you a better idea of why this is such a worthwhile route to take.

Attorney Advertisement: This content is for informational purposes. Past results do not guarantee future outcomes. Our practice focuses on traffic and DUI defense across Florida. Office in Broward. Submitting information via our website does not create an attorney-client relationship.

Explore Other Protective Measures

Beyond fighting the ticket, you have other avenues that can help soften the blow, especially if this is your first offense or you have an otherwise clean record.

Elect Traffic School: In Florida, drivers who are eligible can opt to complete a Basic Driver Improvement course. Once you successfully finish it, the state won't add points to your license for that violation. This is a key step in preventing an insurance increase.

Ask About Forgiveness Programs: Some insurance carriers offer "accident forgiveness" or "minor violation forgiveness" programs, especially for loyal customers with great driving histories. It never hurts to call your agent and see if you qualify.

Keep Your Driving Record Clean: Your overall history is a huge factor. If this is your first ticket in years, the impact will be much less severe. Keeping your record spotless from here on out is the best long-term strategy to ensure your rates eventually come back down.

By exploring these options, you shift from a reactive position to a proactive one. Instead of just accepting the consequences, you can actively work to minimize the financial fallout and keep your insurance affordable.

Your Top Questions About Florida Tickets and Insurance

Let's clear up some of the confusion that comes after a speeding ticket. Here are a few of the most common questions Florida drivers ask us about how a citation is going to hit their car insurance.

Do I Have to Tell My Insurance Company I Got a Speeding Ticket?

No, you're not required to pick up the phone and report a speeding ticket to your insurance agent. But that doesn't mean they won't find out.

Insurance companies almost always pull your driving record when your policy is up for renewal. When they get that report from the Florida DHSMV, the conviction will be right there for them to see, and that's usually when they'll adjust your premium.

Will a Ticket from Another State Affect My Florida Insurance?

Yes, that out-of-state ticket will almost certainly follow you home. Florida is part of the Driver License Compact (DLC), which is basically an agreement between most states to share driver information.

This means a speeding ticket you get in another member state gets reported back to Florida. It can then be added to your record and may affect your insurance rates just like a ticket you got locally.

Here's the key takeaway: simply paying a fine—whether in Florida or another state—is an admission of guilt. That's what puts the conviction on your record for your insurer to find.

Is It Worth Contesting a Speeding Ticket in Broward County?

While every situation is different, fighting a ticket in a busy area like Broward County is usually a smart financial move. That initial fine is often just the tip of the iceberg.

A conviction can lead to an insurance rate increase that costs you hundreds or even thousands of dollars over the next three to five years. By fighting the ticket, you give yourself a shot at getting it dismissed or reduced to a non-moving violation, which can prevent points and the insurance hike that follows. The best way to know your options is to talk to a legal professional who handles traffic cases. Our goal is to protect your license and record.

Past results do not guarantee future outcomes.

Can My Insurance Company Drop Me After One Speeding Ticket?

It's pretty rare for an insurance company to cancel your policy or refuse to renew it after a single minor speeding ticket, especially if you have a clean driving record otherwise.

However, non-renewal becomes a real possibility if the ticket is for something serious, like excessive speed (think 30+ mph over the limit) or reckless driving. It can also happen if this new ticket creates a pattern of risky behavior on top of other recent violations on your record.

For more detailed answers, you can check out our comprehensive Florida traffic ticket FAQs to get the information you need.

Don't let a speeding ticket dictate your insurance rates for the next five years. Ticket Shield, PLLC handles traffic ticket matters across Florida. Our practice focuses on protecting your driving record and keeping your premiums down. Get your free consultation today at https://www.ticketshield.com.