How Does a DUI Affect Car Insurance: How a DUI Affects Your

A Florida DUI arrest is serious. Learn how does a dui affect car insurance rates, coverage, & SR-22 requirements. Protect your record. Call us.

A Florida DUI can wreck your insurance, but the worst damage usually follows a conviction, not just an arrest. Act fast. A strategic defense under Florida Statute § 316.193 can protect your license, your record, and your future insurance costs.

You were just arrested. Your car may have been towed. Your phone is full of missed calls. You’re trying to figure out what happens next, and one question keeps coming up: how does a dui affect car insurance?

Here’s the direct answer. A DUI conviction is what usually triggers the biggest insurance fallout. That’s when insurers treat you as a high-risk driver, strip away favorable pricing, and make coverage harder to keep or replace. An arrest is serious, but it is still a charge. That distinction matters. A lot.

That’s why your first move shouldn’t be panic. It should be defense. If you need a plain-English overview of what happens after an arrest, start there, then focus on the part often ignored early: protecting your driving record before a conviction locks in the insurance damage. For a broader Florida-focused look at the legal fallout, review these consequences of a DUI.

Table of Contents

Your Guide to Navigating a Florida DUI

A Florida DUI case moves fast. The legal risk is obvious. The insurance risk sneaks up on people later, often when renewal paperwork arrives and the premium jumps. By then, your bargaining power is gone.

Florida DUI cases are governed by Florida Statute § 316.193. If your case is headed into a courthouse like the Richard E. Gerstein Justice Building in Miami-Dade, you need to treat every early decision as important. What you say, what you sign, and whether you challenge the case promptly can change the outcome.

Why should you care about insurance this early

Because insurance companies price risk based on what lands on your driving profile. If you let this case drift toward a conviction, you’re not just dealing with court penalties. You’re setting up years of expensive insurance consequences.

Practical rule: Don’t treat insurance as a later problem. In a DUI case, insurance protection starts with criminal defense strategy on day one.

A lot of online advice makes a quiet but dangerous assumption. It assumes conviction is inevitable. That’s bad advice. You need to think the opposite way. Your goal is to prevent the outcome that causes the worst insurance consequences in the first place.

What should your mindset be right now

Be controlled. Be quiet. Be organized.

You don’t need ten opinions from friends. You need a plan tied to the facts of your stop, the testing, the officer’s observations, the paperwork, and the timeline. A DUI arrest can still be challenged. Evidence can be attacked. Procedures can be questioned. That work matters because insurance companies react most strongly when a major violation is established, not when you’re merely accused.

Use the next hours and days to protect three things:

Your license

Your driving record

Your insurability

If you keep those in focus, you’ll make better decisions than someone who only reacts to the criminal charge.

What Immediate Actions Will Your Insurer Take?

Your insurer usually won’t rewrite your life overnight just because you were arrested. But don’t get comfortable. Carriers monitor risk, and a DUI allegation can put your policy under a microscope.

Will your insurer react to an arrest or wait for a conviction

An arrest and a conviction are not the same event. That distinction matters to your insurer, and it matters to your defense.

After an arrest, your insurer may do very little immediately. Many carriers won’t make a major underwriting move until there’s an official record they treat as a major violation. But that doesn’t mean nothing is happening. Internal review can begin. Your renewal file can get flagged. Questions can arise if there was an accident, a license issue, or a required filing later on.

A conviction changes the situation. That’s when insurers are far more likely to reevaluate whether they want to keep you, renew you, or move you into a more expensive risk tier.

A DUI file is often quiet before it gets expensive. Silence from your insurer right after an arrest doesn’t mean you’re safe.

What notices should you watch for right now

Watch your mail, email, and policy portal carefully. Don’t ignore routine-looking insurance correspondence. Important notices often arrive in ordinary packaging.

Focus on these issues:

Policy review activity

Your carrier may review your eligibility, especially if the DUI arrest involved a crash, injuries, or another serious allegation.Renewal changes

A company that doesn’t cancel mid-term may still decide not to offer the same terms at renewal.Requests for updated information

If your license status changes or a court outcome posts, your insurer may require updated records or proof of compliance.High-risk placement pressure

If standard coverage becomes harder to maintain, you may be pushed toward less favorable options.

The key mistake is passivity. Don’t wait for insurance paperwork to explain your legal reality to you. By then, your defense window may have narrowed.

What should you do before your insurer acts

Keep your current policy active. Don’t let it lapse. Don’t assume you can fix a gap later without consequences.

Also, don’t volunteer unnecessary statements to your insurer about the criminal case. Give required information if needed, but don’t turn a legal defense problem into an avoidable admissions problem. Let your lawyer guide that communication.

How Much Will Your Car Insurance Rates Increase?

If you’re convicted, the financial damage can be severe. This is the part drivers underestimate until the bills arrive.

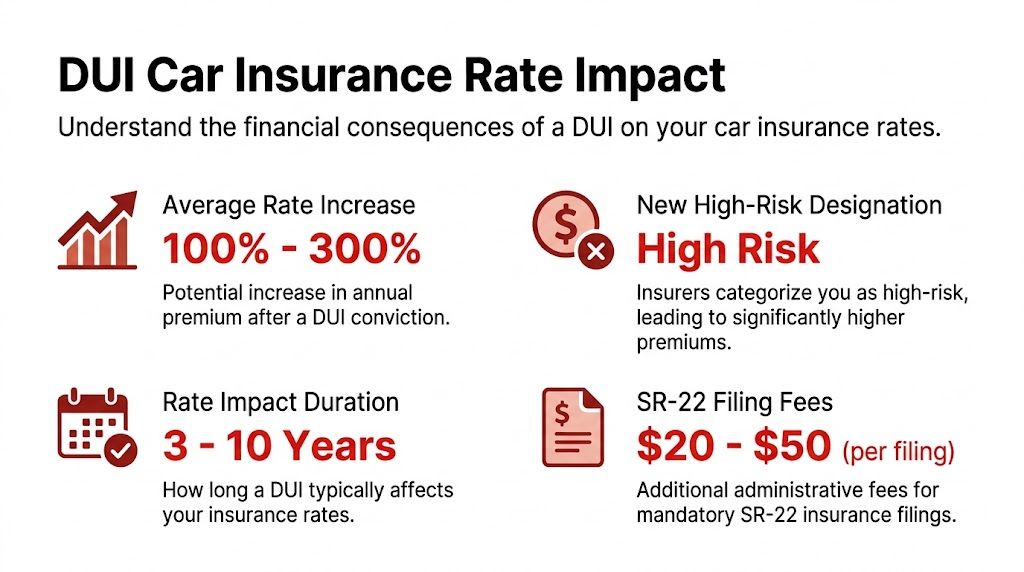

A DUI conviction typically causes substantial premium increases ranging from 80% to 200% or more, and many drivers see their insurance costs double or even triple over the following years, according to this DUI insurance analysis. The same source explains that a driver paying $1,200 annually may see that cost rise to $2,400 or $3,600 after a conviction.

What does a conviction usually cost

The short answer is this. Much more than is commonly expected.

According to that same analysis, those higher premiums can add up to thousands of dollars in additional insurance expenses over a three to five-year period. That’s before you factor in the broader pressure that comes with being pushed out of preferred pricing.

If you want to understand how insurance pricing punishes even less serious driving issues, compare it with the cost of insurance increase after a Florida speeding ticket. A DUI is in a different category entirely.

Why do insurers raise rates so aggressively

Because they don’t price a DUI as a minor mistake. They price it as a major risk event.

The source above states that insurers classify DUI offenders as high-risk drivers. That reclassification has consequences beyond the headline premium increase:

Loss of preferred rates

You stop being treated like a lower-risk driver with a favorable pricing profile.Discount problems

Good-driver style savings can disappear.Higher deductibles and limited options

Coverage can become harder to structure on favorable terms.Coverage refusal from some insurers

Some companies may decline to insure drivers with a DUI record, forcing them toward specialized high-risk carriers.

Why the defense cost comparison matters

Drivers often focus on the upfront cost of legal representation and ignore the longer insurance tail. That’s backwards.

Financial reality: A weak defense can cost you in court. A failed defense can keep costing you every renewal cycle after that.

If you’re asking how does a dui affect car insurance, the honest answer is brutal. A conviction can alter your pricing, carrier options, and policy terms for years. That’s why the case has to be fought early and strategically.

What Is an SR-22 and How Long Do You Need It?

An SR-22 is not a separate insurance policy. It is a certificate of financial responsibility filed by your insurer to show the state that you carry the required coverage.

In Florida, this issue connects directly to Florida Statute § 316.193, the DUI statute. After a DUI conviction, the state can require compliance steps tied to restoring and maintaining lawful driving status. For many drivers, that means dealing with the SR-22 requirement as part of the fallout.

What is an SR-22 in Florida

The SR-22 tells the state that your insurer is backing your coverage and can alert the state if that coverage drops. It puts your insurance status under tighter supervision.

Following a DUI conviction in Florida, you will be required to file an SR-22 for three years, and insurers will consider the DUI a major violation affecting rates for at least three to five years, sometimes longer, according to Allstate’s explanation of how DUI impacts car insurance.

That matters for two reasons. First, the filing itself is a practical burden. Second, it keeps the DUI tied to your driving profile in a way insurers pay close attention to.

How long will it affect you

The legal filing period and the insurance pricing period are not always identical.

Allstate notes that a DUI may remain on your driving record for 3 to 10 years depending on the state, and insurers typically treat it as a major violation for three to five years, though some may consider it for up to a decade. The same source says rates can gradually decrease if you maintain a clean record and avoid additional tickets or accidents.

For Florida drivers, that means the SR-22 obligation may end before the insurance consequences fully fade.

If you’re also trying to stay mobile for work, review the practical licensing issues around a DUI hardship license in Florida.

A short explainer can help if the filing process feels abstract:

What should you do if SR-22 becomes part of your case

Handle it carefully and without delay.

Confirm the requirement

Don’t assume. Verify exactly what Florida requires in your case.Use an insurer that understands filings

Not every carrier handles these situations smoothly.Keep coverage continuous

A lapse can create a new problem fast.Stay violation-free afterward

Clean driving behavior helps when insurers eventually reassess your risk.

How Can You Mitigate the Insurance Impact of a DUI?

The strongest way to protect your insurance is simple. Fight the case before it becomes a conviction.

Most drivers get this backward. They think about insurance shopping after the fact. That’s too late. The true advantage comes from the legal outcome.

Why the arrest versus conviction difference matters

An arrest is an accusation. A conviction is a formal result with far more serious insurance consequences. If you remember only one thing, remember that.

Here’s the practical comparison:

Event | Impact on Car Insurance |

|---|---|

DUI Arrest | Serious warning sign. Your insurer may review your file, but the most damaging long-term pricing consequences usually depend on what is ultimately entered on your driving record. |

DUI Conviction | Major insurance event. You face high-risk classification, premium spikes, reduced carrier options, and possible filing requirements tied to maintaining lawful coverage. |

That’s why strategy matters immediately. A careful defense can challenge the stop, the officer’s observations, field sobriety issues, breath or blood testing, and procedural errors. In some cases, the goal is dismissal. In others, it’s reduction to an outcome that avoids the same insurance catastrophe.

If you want to understand what that fight can look like, review how to get DUI dismissed.

The insurance system punishes convictions much harder than allegations. Your legal strategy should be built around that reality.

Who gets hit hardest by the insurance fallout

Generic DUI advice fails a lot of Florida drivers because the actual impact is not the same for everyone.

According to this discussion of DUI insurance consequences by driver profile, the financial impact varies dramatically based on who you are. Younger drivers, gig workers, and military personnel can face disproportionate rate hikes and career-related consequences.

That profile-based risk matters in Florida:

Gig drivers may lose the ability to keep driving for income.

Military personnel may face record-related consequences beyond simple transportation issues.

Younger drivers can get boxed into very expensive coverage options.

Why automated help isn’t enough

A DUI defense is not a form submission problem. It is not something a chatbot, middleman, or volume-driven ticket operation can solve with a canned workflow.

You need a lawyer who looks at your facts and builds a position. Was the stop lawful? Was the testing handled correctly? Were there inconsistencies in the report? Did the state overcharge the case? Those questions affect outcomes. Outcomes affect insurance.

If your defense is generic, your result may be generic too. And generic results are expensive.

What Are Your Immediate Next Steps in Florida?

If your case is heading into a courthouse like the Edgecomb Courthouse in Tampa, time matters now. Not next week. Not after you “see what happens.”

Florida DUI cases create two urgent tracks. The criminal case under § 316.193 and the license consequences that can start almost immediately. If you move slowly, you give away options.

What should you do in the next few days

Take these steps now:

Stay silent about the facts of the case

Don’t explain, justify, or try to talk your way out of it with police, investigators, or anyone else who can repeat your words later.Preserve every document

Keep the citation, bond paperwork, tow receipt, property sheet, and any temporary driving permit in one place.Write down what happened

While it’s still fresh, note the stop location, timeline, what the officer asked, what tests were requested, and what you said.Protect your license quickly

Florida deadlines come fast after a DUI arrest. Delay can cost you a meaningful chance to challenge the administrative side.Keep your insurance active

Don’t create a second problem with a lapse in coverage.Get legal guidance immediately

Fast review of the stop, testing, and paperwork can shape the entire defense.

For a practical overview of the early legal process, read what happens after a DUI arrest.

Waiting is a decision. In a DUI case, it’s usually the wrong one.

The right move is focused action. Protect the record. Protect the license. Protect the insurance profile before a conviction hardens everything against you.

If you were arrested for DUI in Florida, speak with a real lawyer now, not an automated app or a ticket mill using middlemen. Ticket Shield, PLLC is a lawyer-led Florida defense firm where you can speak directly with your attorney by phone or text. Get a free consultation and fight for the outcome that matters most: No Points, no unnecessary damage to your license, and no avoidable insurance fallout.