Understanding Florida Traffic Accident Laws: Your Guide to Protection

Florida traffic accident laws can be confusing. Understand your rights, the no-fault system, and strict deadlines to protect your case after a crash.

You are legally required to stop, render aid, and exchange information after any accident. Under Florida Statute § 316.062, leaving the scene of a crash involving injury is a felony. Reporting any crash with over $500 in damage is also mandatory. Protect yourself immediately.

What Are My Immediate Legal Duties After A Crash?

The minutes after a crash are chaotic. Adrenaline is high. Confusion is normal. But Florida law demands specific actions from you. Failure to comply can turn a bad day into a legal disaster. Your license, your finances, and your freedom are on the line.

Your priorities are clear. Keep everyone safe. Fulfill your legal duties. The steps you take now build the foundation for your defense.

What Immediate Steps Must I Take?

These are not suggestions. They are your legal responsibilities under Florida law.

Stop Your Vehicle. Never leave the scene of an accident. Pull over safely. Fleeing is a serious crime.

Render Aid. You have a legal duty to provide "reasonable assistance" to anyone injured. This means calling 911 immediately.

Exchange Information. You must provide your name, address, and vehicle registration number. You must also show your driver's license.

Report the Crash. You must report any crash with injuries or apparent property damage of $500 or more to the police. This is non-negotiable.

What is the Most Common Mistake to Avoid?

Do not admit fault. This is a critical error.

Simple phrases like "I'm so sorry" or "I didn't see you" will be used against you. Insurance companies and lawyers will twist your words. Stick to the facts. Give only the required information to law enforcement.

The side of the road is now a high-stakes legal environment. Every word you say can become evidence against you. One mistake can jeopardize your entire defense.

This is where direct attorney access is critical. Automated apps leave you to face this alone. At Ticket Shield, PLLC, you get a direct line to your lawyer via phone or text. We provide urgent, strategic guidance the moment you need it. We protect you from making a costly error when you are most vulnerable.

How Does Florida's No-Fault System Really Work?

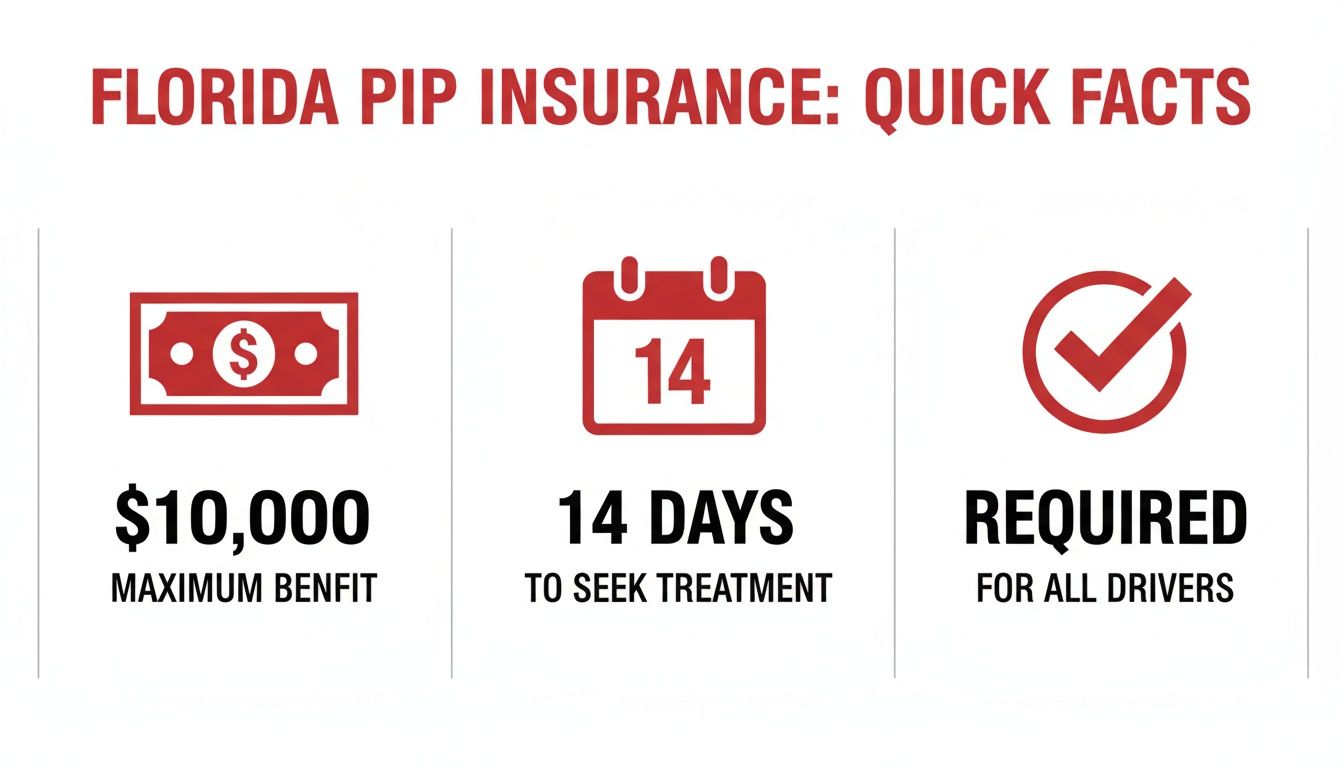

Florida's "No-Fault" law means your own PIP insurance covers your first $10,000 in medical bills. But you have a strict 14-day deadline to seek medical care after the crash. If you miss this window, your PIP benefits can be denied completely.

The term "No-Fault" is dangerously misleading. It suggests no one is held responsible. That is wrong. The system is a minefield of deadlines and limits that can leave you with massive bills. You must understand how it operates to protect yourself.

The purpose of No-Fault is to get initial medical bills paid quickly. It uses your own insurance first. This avoids long delays while fault is determined. It does not mean the at-fault driver is off the hook.

What is Personal Injury Protection (PIP)?

Under Florida Statute § 316.066, every driver must carry a minimum of $10,000 in Personal Injury Protection (PIP). This is the core of the no-fault system.

PIP is your emergency medical fund after a crash. It covers a portion of your medical bills and lost wages immediately. It pays out regardless of who caused the accident.

But this coverage has a brutal, non-negotiable deadline.

You must seek initial medical treatment within 14 days of the accident. Miss this 14-day window, and your insurer can legally deny all your benefits. You will receive nothing.

This deadline is absolute. Injuries can take days to appear. Waiting to see a doctor is a catastrophic financial mistake.

What is the Difference Between PIP and Bodily Injury (BI)?

Confusing these two coverages is a costly error. You must know the difference.

Personal Injury Protection (PIP): This is for you. It covers your own initial medical costs and some lost wages up to the $10,000 limit.

Bodily Injury (BI) Liability: This is for others. If you cause a crash, BI pays for the injuries you caused to someone else. It protects your assets.

The danger is that BI coverage is not mandatory for all Florida drivers. This creates a huge risk. If a driver without BI hits you, and your medical bills exceed your $10,000 PIP limit, you may have no way to get your bills paid.

Property damage is a separate issue. You need to understand what happens when a vehicle is totaled and gets a What Is Salvage Title.

Do not try to navigate these insurance rules alone. An app uses chatbots, not lawyers. At Ticket Shield, you speak directly to your attorney. We provide the strategic advice you need to meet every deadline and protect your rights.

How Can The 51% Fault Rule Affect My Claim?

A 2023 law change means if you are found 51% or more at fault for a crash, you are legally barred from recovering any money from the other driver's insurance. This rule is a financial trap, and insurance companies are using it to deny claims.

A recent change in Florida law completely changed how financial recovery works after a crash. This is not a minor tweak. It is a financial cliff. Insurance adjusters now have a powerful weapon to deny your claim.

This new system is called modified comparative negligence. We call it the 51% Bar Rule. Before this change, you could still receive some compensation even if you were mostly at fault. Not anymore.

What Is The 51% Bar Rule?

The rule is brutally simple. After a crash, insurance companies assign a percentage of fault to each driver. Your ability to get paid is tied directly to that number.

If you are found 0% to 50% at fault, you can recover damages. Your payout is reduced by your percentage of fault.

If you are found 51% or more at fault, your recovery drops to $0. You get nothing for your injuries or vehicle damage from the other party.

Your PIP insurance provides a small, initial cushion with strict limits.

While your PIP gives you a $10,000 head start (if you seek treatment within 14 days), that money is exhausted quickly in a serious injury. You are then exposed to the harsh reality of the 51% Bar Rule.

How Do Adjusters Use This Rule Against You?

Insurance companies are not your friends. Their goal is to pay you as little as possible. The 51% Bar Rule is their best tool. An adjuster's entire strategy is to push your share of blame over that 51% line.

They will dissect the police report. They will twist your recorded statement. They will hunt for any detail—a moment of distraction, a slightly worn tire—to argue you were mostly at fault.

This is a daily battle fought in courtrooms like the Edgecomb Courthouse in Tampa.

Imagine you have $100,000 in damages. See how your potential recovery changes under the old rule versus the new 51% rule.

How The 51% Bar Rule Impacts Your Recovery

Your Percentage Of Fault | Damages Awarded (Old Rule) | Damages Awarded (New 51% Rule) | Financial Impact |

|---|---|---|---|

30% At Fault | $70,000 | $70,000 | No change. Your award is reduced by your 30% fault. |

50% At Fault | $50,000 | $50,000 | No change. Your award is reduced by your 50% fault. |

51% At Fault | $49,000 | $0 | Catastrophic. You go from a significant recovery to nothing. |

75% At Fault | $25,000 | $0 | Total loss. Under the old rule, you still recovered something. Now, it's zero. |

As you can see, crossing the 51% threshold is devastating. Insurance companies know this. They will use it against you.

You cannot fight this system with a chatbot or a middleman. You need a dedicated legal defender. At Ticket Shield, PLLC, you speak directly with your attorney. We build a defense from day one to fight back against unfair blame and protect your rights.

When Am I Legally Required To Report An Accident?

Under Florida Statute § 316.065, you must report any accident involving injury, death, or apparent property damage over $500. A handshake deal is not enough. Failing to report can lead to severe penalties, including hit-and-run charges.

After a minor crash, it is tempting to avoid the police. You might try to handle it with a handshake. This is a dangerous and often illegal mistake.

Knowing when to report a crash is a legal command. A verbal agreement means nothing. The other driver can change their story later. A police report is your official shield. It creates an unbiased record of what happened.

What are the Legal Thresholds For Reporting?

Florida law is specific. You must immediately report a crash to local police or the Florida Highway Patrol if it involves any of the following:

Any Injury or Death: This is non-negotiable. Even a minor complaint of pain triggers your duty to call 911.

Property Damage Over $500: A small dent on a modern car costs thousands to repair. Nearly every collision meets this $500 threshold.

A Hit-and-Run: If the other driver leaves, you must report it immediately to protect yourself.

An Impaired Driver: If you suspect the other driver is under the influence, reporting is mandatory.

A Commercial Vehicle: Crashes with commercial vehicles have specific reporting rules that you must follow.

What are the Consequences of Not Reporting?

Failing to report a crash is a massive error. Leaving the scene of an accident is a "hit-and-run." Florida treats this crime with extreme severity.

What seems like a simple traffic matter can escalate into a felony charge. High-stakes legal battles over these charges play out at the Broward County Judicial Complex in Fort Lauderdale—a place you want to avoid.

A formal crash report is your primary defense. It documents key facts and protects you from false claims.

An official report locks in the details. It prevents the other driver's story from changing. It provides critical evidence that a lawyer-led firm like Ticket Shield uses to defend you. Without it, your case becomes your word against theirs.

Automated apps leave you alone to make this critical decision. At Ticket Shield, you get direct access to your attorney. When you text or call, you get immediate advice on your reporting duties. We ensure you do everything right to protect yourself from the start.

What Is The Deadline For Filing An Accident Lawsuit?

Warning: Florida law has changed. For most accidents after March 24, 2023, you now have only TWO years to file a personal injury lawsuit, not four. If you miss this deadline, your right to seek compensation is lost forever. You must act quickly.

Time is your enemy after a car accident. The legal system runs on strict deadlines called statutes of limitations. For Florida drivers, the time to file a lawsuit has been cut in half.

This is a hard cutoff. If you miss this deadline by one day, the courthouse doors are locked. Your right to pursue financial compensation vanishes. Insurance companies know this. They will delay and drag out negotiations, hoping you run out of time.

What is the New Two-Year Deadline For Negligence?

For any accident on or after March 24, 2023, you have just two years from the date of the crash to file a lawsuit. This is a dramatic change from the old four-year deadline.

This two-year deadline, established under Florida Statute § 95.11, puts immense pressure on you to act fast. For crashes that occurred before that date, the old four-year statute of limitations still applies.

Do not wait. Building a strong case takes time. You must gather evidence, find witnesses, and fight with insurance adjusters. The clock starts ticking the second the crash happens. Two years will disappear quickly.

Immediate action is not just a good idea. It is essential to protecting your legal rights.

Are All Legal Timelines The Same?

No. Different claims have different deadlines. This is a dangerous point of confusion.

Personal Injury (Negligence): A strict two-year deadline for any accident after March 24, 2023.

Property Damage: You have four years to file a lawsuit for damage to your vehicle.

Wrongful Death: A family has two years from the date of a loved one's passing to file a lawsuit.

These timelines are separate from traffic ticket deadlines. We explain those in our guide on the statute of limitations for traffic violations in Florida.

Keeping these deadlines straight is treacherous. An app cannot provide the strategic counsel needed to preserve your claim. At Ticket Shield, you speak directly with your attorney. We ensure every deadline is met, protecting your case from being dismissed on a technicality.

Why Choose A Lawyer-Led Firm Over An Automated App?

After a crash, you need expert legal advice. This is no time for chatbots, middlemen, or automated "ticket mill" apps. An algorithm cannot negotiate with a prosecutor. It cannot build a compelling legal argument. It cannot protect your rights.

Your case needs human strategy. It demands the insight that only comes from years of experience inside Florida courtrooms like the Richard E. Gerstein Justice Building in Miami.

What is the Problem With Automated Systems?

Automated legal apps are built for volume, not results. They treat you like a case number. You deal with customer service agents, not your actual attorney. A wall is placed between you and the person defending you.

These transactional systems cannot:

Give you immediate, personalized legal advice. You need a lawyer on the phone, not a chatbot, when you are on the side of the road.

Listen to your story. An app cannot spot the critical details in your account that could win your case.

Negotiate with prosecutors. Getting a charge reduced requires a professional legal argument, not a generic form letter.

Stand with you in court. You need an experienced attorney by your side, not a defense processed by a machine.

An app is a transaction. Hiring a lawyer is an act of protection. When your driving record and financial future are at stake, a simple transaction is never enough. You need a dedicated legal shield.

What is the Ticket Shield Difference?

At Ticket Shield, PLLC, our entire model is built on one powerful promise: you speak directly to your attorney.

When you hire our firm, you get your lawyer’s direct cell phone number. You can call or text them. There are no middlemen. No case managers. No gatekeepers. Your direct line to your attorney is your most powerful asset.

This direct access is the core of our strategy. It allows us to understand your case, provide real-time guidance, and build the strongest defense possible. To understand more, learn about why choosing a local lawyer over an app is the most important decision you can make.

This is not a transaction. It is a dedicated legal defense. An app cannot match the strategy and protection that comes from having an experienced Florida traffic attorney in your corner.

What are the Answers to My Most Urgent Questions?

Quick answers: Uninsured Motorist coverage is for crashes with uninsured drivers. Yes, you can be sued personally if damages exceed your insurance limits. You must report any crash with injuries or damage that appears to be over $500.

What If The Other Driver Is Uninsured?

This is why you need Uninsured Motorist (UM) coverage. Your own UM policy pays for your damages when the at-fault driver has no insurance. Without UM coverage, your options for recovery are extremely limited. You must speak with an attorney immediately to explore any remaining paths to get your bills paid.

Can I Be Sued Personally For An Accident In Florida?

Yes. If the damage you cause exceeds your Bodily Injury (BI) liability limits, the other party can sue you personally. They can pursue a judgment against your personal assets—your savings, your home, your future income. Sufficient BI coverage is a financial shield that protects you from one bad day on the road.

Do I Have To Report A Minor Fender-Bender?

Under Florida Statute § 316.065, the law is clear. You must report any crash involving an injury or property damage that appears to exceed $500. Given the high cost of modern vehicle repairs, almost any collision will meet this threshold. Reporting the crash is always the smartest way to legally protect yourself.

An accident also impacts your car's resale value. It is important to learn how to calculate diminished value and win your claim.

At Ticket Shield, PLLC, you speak directly with your attorney. You get clear answers and a strategic defense. We fight to protect your record and your future.

To protect your record and fight for no points, visit TicketShield.com for a free consultation.